Is Connected Fitness Dead?

Is Connected Fitness Dead?

At-home connected fitness saw explosive growth in 2020 due to Covid-induced lockdowns, but 2021 has been a different story. Is connected fitness a true multi-decade secular growth story, or a fad?

Happy Monday! 👋

This is going to be a fun one! With the recent turbulence in Peloton’s stock price after a dismal Q122 earnings release (chart below), many once-avid connected fitness bulls are beginning to wonder: Is Connected Fitness Dead?

From the looks of this chart, one could draw the conclusion that at a very minimum, Peloton as a company is in trouble. However, as World economies are re-opening and getting back to somewhat normal, the headwinds that many connected fitness companies are experiencing are very real and the impact is being felt beyond just Peloton.

Evidence of a much more challenging environment is plentiful:

On 10/7/21, iFit Postpones IPO as volatility concerns grow.

After peaking above $15.50 on 2/22/21, Beachbody’s stock has collapsed to below $5.00 at the time of this writing.

In their most recent earnings calls, both Nautilus and Peloton mentioned “global supply chain” constraints as negatively impacting their business.

In Peloton’s Q122 earnings call, they also mentioned privacy changes made by Apple that “are leading to some targeting headwinds”. Whispers amongst the connected fitness space have indicated similar issues, resulting in an increase in Cost of Acquisition (CAC) and lower margins.

During Q421 earnings call, Peloton cut the price on their OG Bike. CEO John Foley emphasized that this was an offensive move to make it a no brainer purchase relative to competition, but many feared that this was a move of desperation due to low demand. Fears stoked an all-time high in Q122 earnings release when management stated “it is clear we underestimated the reopening impact on our company and the overall industry.”.

Reading the bullets above, one could quickly conclude that the connected fitness industry could have been nothing but a mirage created by Covid-induced lockdowns.

However, a quick check on Google Trends paints a picture that demand certainly was at an all-time high during the pandemic, but is continuing to remain elevated:

Industry L12 Months:

Peloton YoY:

In this sub, I’ll take a deep dive into the beginning of connected fitness, the Peloton Effect, the current state of connected fitness, the Great Rebalance and what I think the future holds.

Enjoy!

Myles

Disclaimer: This is not investment advice. I am not a registered investment adviser. I don’t know where any of the public companies mentioned will price. You should do your own research.

Let’s get to it.

The Beginning of Connected Fitness

TL;DR timeline infographic can be found below:

Group exercise first became popular in the 1960s when the term “aerobics” was coined. A physician by the name of Kenneth Cooper penned a book that used science to make a compelling case as to why fitness was beneficial to one’s health. Fast forward a decade to the 1972 olympics, an event that left the US enamored by distance running due. This was due to the dramatic finish of the men’s marathon, where Frank Shorter overcame a vigilante running on the course in an effort to distract him from winning the race. He still took home gold, and the rest of America took notice. Meanwhile in the 70s, Jazzercise was invented by Judi Missett which really laid the groundwork for the event boutique fitness boom of the 2000s.

While all of the key milestones were important, the most notable piece of connected fitness history occurred in 1982 when Jane Fonda created the VHS at-home workout video, “Jane Fonda’s Workout”. While the title was unoriginal, the concept was novel. Leveraging newer VHS technology that was invented in 1976, Jane pioneered the at-home workout experience. It was the first non-theatrical home video release to ever top sales charts. Also during the 80s, big box gyms became increasingly popular, sometimes being dubbed the modern country club. In typical US consumer fashion, attractiveness of big eventually ebbed to being enamored by small. Minimalist Yoga studios and 1:1 personal training sessions started to become more mainstream.

Ultimately, the 1980s at-home workout boom and the 1990s mass Yoga adoption were the two critical ingredients that lead to the boutique fitness boom of the 2000s, and eventually technological disruption that the fitness industry had never seen via connected fitness. One may think that all of the pieces were in place at this point for connected fitness to be introduced. However, the key and final ingredient really had nothing to do with fitness. In 2007, Netflix introduced media streaming and on-demand content. The fitness industry had no clue at the time, but with this move, Netflix would indirectly and unknowingly completely disrupt the fitness industry as we know it.

In 2012 with the founding of Peloton, John Foley and Tom Cortese created the first S Curve Shift that the fitness industry had seen since Jane Fonda leveraged VHS technology in the early 1980s. Peloton would go on to reshape the fitness industry by leveraging media streaming and on-demand content to bring the cycling studio experience directly into your home.

The Peloton Effect

It took several years before the World really started to learn about Peloton. With the Covid-induced lockdowns in early 2020, if you didn’t know about Peloton by then, well now you did. As the World scrambled to stay in shape with gym doors shuttered, adoption of Peloton’s products shot to the moon. In general, the adoption of at-home connected fitness experienced tailwinds that industries rarely ever see. What was already a rapid secular adoption of this burgeoning new technology, now had become hyper-adoption to the point that backlogs for at-home fitness products swelled to over 3 months at times.

Regardless of when you first learned of Peloton, when you met someone who Peloton’ed, you immediately knew it. While current sentiment around Peloton’s stock is as low as it has ever been, you wouldn’t know it by talking to their customers. Peloton’s product, content and brand have created a cult-like following only seen with brands such as Tesla and Apple. Put simply: People that use the product are obsessed.

From 2015 through 2020, the company grew revenue by over 100%. It has consistently boasted a 90+ NPS score, and churn is the lowest that the fitness industry has ever seen at over 90% annual retention.

This insane growth and stickiness has ultimately led to several new competitors, and more importantly, venture and growth capital tailwinds. These capital tailwinds have led to exciting new innovations within the connected fitness space in a very short amount of time.

All of this is what I have coined The Peloton Effect.

The Peloton Effect goes beyond just capital investments, though. With the creation of new technologies and immersive content, a new class of innovators has been created, and they are capturing the attention of the consumer in a way that the industry has never seen. Read through comment threads on Peloton Facebook or Instagram posts, and you’ll find a cult following craving more products, new content, and overall new ways to work out and stay fit. Go to pitch competitions or fitness/sports technology accelerator programs, and you’ll find applications of AI, Machine Learning, and Virtual & Augmented Reality being applied to new innovative fitness products. You’ll see venture capitalists lining up to invest in oversubscribed rounds with stiff valuations. This is the Peloton Effect, and until recently, it has shown no signs of slowing down.

The Current State of Connected Fitness

So, that brings me to the original purpose of this article: Is Connected Fitness Dead? Gyms and boutique fitness studios are re-opening, people are sick of being at home, and there’s obviously been a massive pull forward in demand for at-home fitness products. Or to the contrary, did Covid simply accelerate the secular shift in consumer behavior that was already happening due to the new connected fitness technology offerings? I believe the latter.

Industry Overview

In order to fully understand if connected fitness is dead or here to stay, you have to understand what it is. The definition of connected fitness is: The application of digital technology to sports, fitness and wellness activities using a “smart” mix of hardware, software, and content. At-home connected fitness is simply a sub-category of the more broad connected fitness category.

One must also understand the types of fitness offerings as they stand today:

Big Box Gyms: Examples include Planet Fitness, Equinox, Lifetime Fitness, and LA Fitness.

Average Monthly Price (US): $37.71

Overview: Big box gyms typically consist of weights, cardio equipment, swimming pools and group fitness classes.

Boutique Fitness Studios: Examples include Orangetheory, CycleBar, Pure Barre, SolidCore, F45, and Shred415.

Average Monthly Price (US): $150 for unlimited classes.

Overview: I like to sub-segment this part of the industry into singular-focused (cycling, barre, yoga) and multi-focused (Orangetheory and Shred415). The latter typically has more equipment and HIIT style workouts that are more difficult to replicate within the home.

At-Home Connected Fitness Products: Examples include Peloton bikes, treadmills and strength (Guide launching in 2022), Ergatta’s gamified rower, Tonal’s strength machine, Mirror’s instructor-led device and Tempo’s strength products. I intentionally don’t call out a lot of the legacy equipment makers that have played copy cat with Peloton and lack innovation (Echelon, Myx and iFit).

Average Monthly Price (US): Varies, but for a Peloton product it ranges from $12.99-$111.17 (Peloton Digital on the low end and Peloton Tread+ on the high end).

Overview: There are many different types of at-home workouts you can do, and I like to sub-segment them into Free (Youtube, Instagram), Digital (Peloton, Apple Fitness), Hardware (Peloton, Tonal, Ergatta, Mirror) and Virtual (Oculus, Holofit).

With Peloton’s new strength offering, the all-in price point is significantly lower ($23.11) than any other paid physical product offering on the market. I think that this is key to really expanding the SAM for connected fitness of the future. Reduce the barriers for the consumer to enter the ecosystem via low cost, light weight hardware, and the connected fitness market has a high likelihood of continuing its disruptive path. Regardless, it doesn’t take a really smart person to see that from a pure economics standpoint, at-home connected fitness products are very compelling relative to boutique fitness studios. I believe this is why most of the products are geared toward that segment of the market vs big box gyms.

Demand Trends

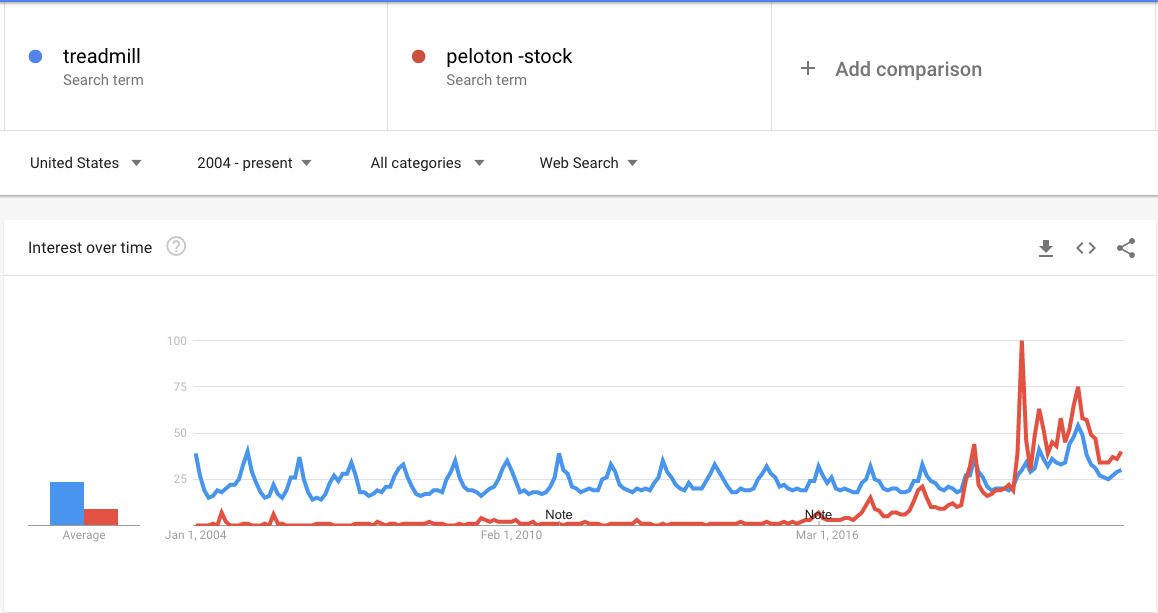

There are tons of different terms that you can search to track current demand trends, but I think it makes sense to look over a long period of time and compare two simple search terms that cast a broad net: “Treadmill” and “Peloton”. Treadmill represents one of the most popular at-home fitness categories over the past several decades, and Peloton represents the leader in connected fitness. These should serve as good proxies for at-home fitness and connected at-home fitness demand search terms.

Likely no surprise here, but search volume for treadmills spikes every year in January. You can also see that Peloton slowly starts creeping up in terms of search volume around the beginning of 2016, but closely mirrors the search trend for treadmill. These trends remained fairly consistent, until December of 2019, when search volume for Peloton far outpaced Treadmill search volume. Remember, the Covid lockdowns would not happen for another 5 months at this point in time, a clear sign that Peloton and the connected fitness boom were taking a strong hold before the pandemic. Since December 2019, Peloton search volume has continued to outpace the most popular at-home fitness category of the past few decades.

This phenomenon indicates to me that not only is demand for at-home connected fitness products still very strong, but that the introduction of new technologies into at-home fitness has increased the total TAM for at-home fitness.

The Fitness Industry

Unfortunately, due to Covid-induced lockdowns, IHRSA reported that 22% of all gyms & fitness studios and 27% of all fitness studios across the US have permanently closed their doors as of July 1, 2021. With a previous count of 41,370 facilities at the end of 2019, IHRSA reported that 29,500 gyms & fitness studios remain as of July 1, 2021. If you have been paying attention like me, you’ve witnessed it in your own neighborhoods, too. Unfortunately, what was already a tough business to turn a profit became extraordinarily more risky to start. This leads me to believe that these numbers will not build back, but rather will continue to decline, especially with the new disruptive technologies that have gone mainstream over the past few years in the at-home connected fitness space.

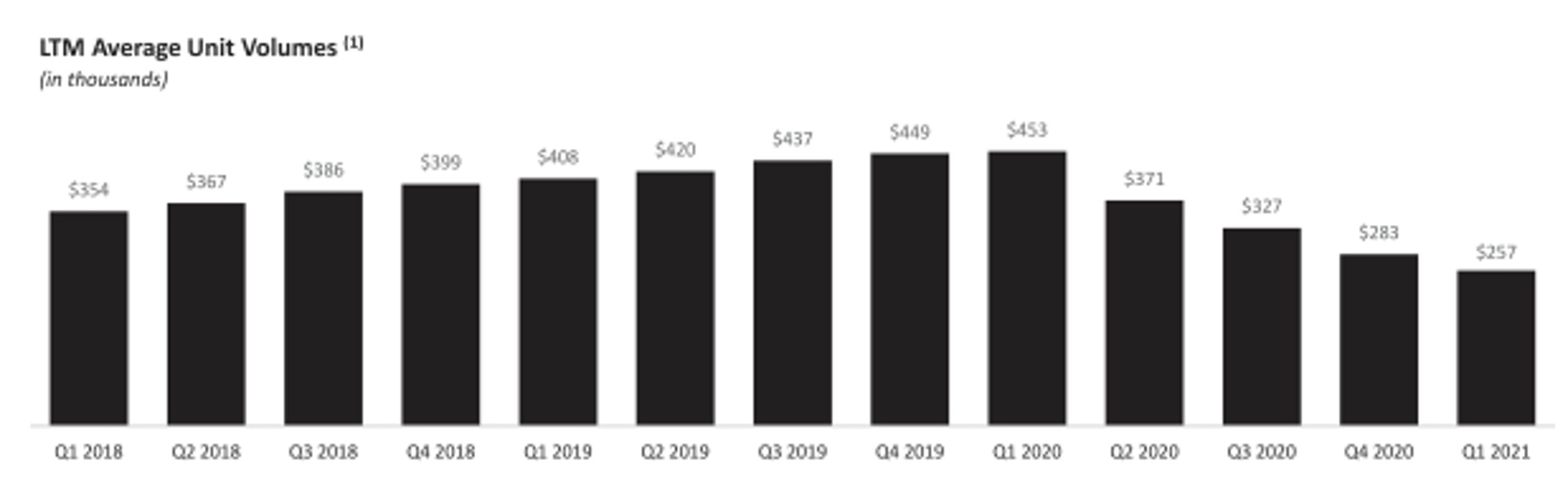

This decrease in overall gyms & fitness studios to attend is going to continue to have a dramatic effect on the industry. With decreased optionality comes further commutes for consumers, decreased class inventory, and lower quality staff as former trainers move on to other more fruitful industries. With most of the business and consumer government stimulus having had ample time to flush through the system, I still think there is more pain to come for the brick and mortar fitness industry. To evidence this assumption, let’s look to one of the largest sources of public boutique fitness industry data that we have: Xponential Fitness. In their S-1 filing, they mentioned that as of May 21, 2021, memberships were 97% of pre-covid levels relative to January 31, 2020. In the same filing, they mentioned that Average Unit Volume (AUV) was 84% recovered. Seems great right?!

Even though in their earnings report, these were both discussed positively, if you dig further, you see a portion of the industry that is still severely damaged and on a further decline. On a 2-year comp basis, Q3 AUV is down nearly 19%, while the total number of fitness studios in the US has decreased approximately 22%. If you multiply the estimated total number of fitness studios in the US as of 2019 and the AUV for Xponential together, and then subtract those numbers from fitness studios remaining as of July 2021, you come to an estimated avg. monthly total volume drop of 37%, or approximately $600M!

Source: Xponential Fitness S-1 Filing

I have a few key takeaways from assessing this data:

Traditional Boutique Fitness is Struggling: The top boutique fitness brands in the US are struggling to get people in their studios to spend money even as the options for consumers has shrunk by 22%. If units go down, but demand is allegedly 97% back to normal, then I’d expect AUV (assuming they have the ability to raise pricing or run more classes) to increase significantly. In a World where #selfcare on Instagram has ballooned from 5M posts in 8/18 to 55.4M posts in 11/21, I think the chances of that many people just being lazy is highly improbable. All of this put together indicates to me that nearly 40% of previous fitness spend is being allocated to other things, including at-home connected fitness devices & subscriptions. This is massive, and creates an unsustainable environment for boutique fitness. Similar to how Blockbuster was able to weather the Netflix storm for a while, Xponential will be able to withstand the attrition being created by disruptive at-home connected fitness forces, but only for so long. It’s clear that at this current trajectory, it’s simply unsustainable and eventually it will catch up to them in a meaningful way.

The Fitness Industry is in Utter Disarray: Both the traditional brick and mortar and at-home connected fitness industries are in a black hole vortex, and it’s anyone’s guess what happens from here. On the brick and mortar side, they’ve lost an estimated $600M of revenue per month. On the connected fitness side, they’ve added net $134M in monthly revenue from hardware and looking at Peloton’s most recent Q1 2022 report, they have about $112M in monthly subscription revenue. Even if you assume that the rest of the connected fitness market has 50% of the subscription revenue that Peloton has, you’re still missing significant revenue from boutique fitness studios, to the tune of approximately $300M per month. So where did this money go? Perhaps it’s going to free fitness services on Youtube or extended free Trials of Apple Fitness/Peloton, but I think there’s a greater dynamic occurring here and we’re still in the thick of it playing out: The Great Rebalance.

The Great Rebalance

We are currently at the pinnacle tipping point of what I am coining the Great Rebalance. As we enter into 2022, most Americans’s fear of Covid is at an all-time low. While some still have high levels of anxiety around the virus, most have resumed a somewhat normal life. But let me make an important point that many people don’t want to admit: Covid is not going away. Similar to how we constantly have to take vaccines for the flu to address new mutations, the same will be said for Covid. Just as we never have eradicated the flu, we will never fully eradicate Covid. In my opinion, the key medical development that will take us closer to normal will take another 12-18 months for mass distribution, which is an antiviral pill that can be easily prescribed and taken orally. Until then, we will have to battle new variants with vaccines and some portion of our population will choose to lay low at times throughout this period.

So, after this is all said and done, we will have been living “new” normal lives for approximately 3-3.5 years. To think that everyone will just simply go back to normal after this long of a period is wishful thinking. To truly answer the question of this article, Is Connected Fitness Dead, we must be able to know what the “new” normal looks like post-covid. What daily habits have changed forever? What products did we invest in or simply try that permanently changed our view of certain activities or behaviors? What new ways of doing things wow’ed us so much that they became critical pieces of our lives? These are very difficult questions to answer, and investors are desperately trying to figure them out. They are trying to find answers with the assumption that we should be back to normal now, which is not the case.

The fact is, we are still trying to figure out what our new normals really are. There are many that did not travel out of fear who are now overcompensating by spending large sums of money on travel experiences. Some are trying to spend as much time outside as possible because they truly quarantined for long periods of time. Some are simply investing more in family events outside of the home because they spent so much money on home renovations and physical goods to enhance their at-home lives throughout Covid.

The point is that the consumer is nowhere near a normal state right now, and the Great Rebalance of our lives is still happening. The dust has yet to settle. When it does, we will have our definitive answer in respect to whether or not connected fitness is dead. Until then, investors will place their bets one way or another on what has grown to be a quintessential battleground industry.

Conclusion

Take the evidence as you will, but it appears that connected fitness is not only alive and well, but it’s growing to become an integral part of our lives. What has been a seasonal slow down in at-home connected fitness products has irrationally snowballed into an all out fear that connected fitness is dead. Just look at Peloton’s valuation for evidence of this. For this example, we’ll use 2020 numbers, not forward looking which is common for a company that has been growing over 100% for almost a decade. Even if you use a 1x multiple on hardware sales, which could be considered fair given that its margins have taken such a big hit of recent, the subscription business of Peloton is being valued at approximately 9.37x.

Next, look at Netflix whose gross margins are comparable to Peloton, and their entire business is being valued around 12x revenue. Further, if you look at a high margin subscription business like Hubspot, and they’re trading at around 35x revenue. Given that Peloton’s churn rates have remained the lowest the fitness industry has ever seen, and extremely low relative to other subscription businesses, I would argue that the multiple on their subscription business should be premium. Regardless, if you use the 12x multiple of Netflix, you have a stock that is undervalued by approximately 23%. If you use a multiple of Hubspot, you are looking at a company that is undervalued by approximately 137%. Note: I recognize that Hubspot is a B2B software company and is likely not the best pure play comp, but the margin profile of the subscription business is comparable.

The markets are not quite pricing in a total death of connected fitness scenario, but it’s pretty close. The key point is that for some reason, it appears that the market is expecting churn numbers to spike rather dramatically, even though there is little evidence to indicate that this will be the case. Go back to before Covid and you will find articles and commentary anticipating churn to increase for Peloton. The fact is, those that have been calling for this to happen are still waiting and have been for years. Is now the time? As the World finds its new normal, perhaps, but I don’t see evidence that supports that position.

In writing this article, my main takeaway is that there is a lot of uncertainty in this industry, and Wall Street generally hates uncertainty. I personally love it. I have a concept that I like to call the “Blackbox Opportunity”. It’s human nature to fear the unknown, but if you are able to stomach the uncertainty of the unknown, a lot of money can be made with blackbox opportunities. I consider the connected fitness space a blackbox type of opportunity, which is why I invested in Ergatta in their pre-seed round and began investing in Peloton as soon as they went public.

Many investors along the way told John Foley, CEO of Peloton, that an industry long known for one hit wonder fads could never produce a unicorn. Here we are nearly 10 years later, with multiple unicorns trading fairly cheaply within a burgeoning multi-decade secular growth story. To this day, the naysayers are still loud and plentiful. The “It’s just a bike with an iPad!” camp have looked like geniuses in 2021, and many think that connected fitness really is dead as a result. I think we’re in the early innings of a generational investment opportunity. Time will tell…

Great article, thanks for sharing. I'm living in South Korea, so sadly I can't try out the Peloton Bike. I really hope affordable home-training devices become the new norm. There are still people who don't understand the subscription pay model (while they agree on additional payments for personal training at fitness centers). Like you've said, as the industry itself changes, the mindset people have will also change, and hardware+subscribing workout programs will become normal.

The best analysis I've ever read on Peloton! Couldn't pass without leaving a comment. Have a good day, Myles.

Myles - Thanks for sharing. Clarifying question: do the search trend charts from the article refer to searching just "peloton" or is it the phrase "peloton stock"? The charts look like they're referencing the latter but I just wanted to confirm.