Introducing The Omnidollar Syndicate

A simple way to access venture capital returns.

Happy Hump Day! 👋

I am beyond thrilled to announce the formal launch of the Omnidollar Syndicate!

Before moving on, the tl;dr version is this:

I am converting my closed investment syndicate to now be open to any accredited investors that would like to participate.

Since I began investing in January 2020, my portfolio of pre-seed and seed round investments has garnered 2.4x in returns (mark-ups).

I have the first investment opportunity secured (I’m very excited about this one). Thus far, about 50% of the $100K allocation is spoken for.

If you’re interested in getting a first look at the investment opportunities that I source through my network, sign up for my syndicate here. Feel free to share this openly with your networks.

Signing up costs nothing and will get you early access to deals that I source before I announce the close of the investments through my normal newsletter.

Okay, now on to the more in depth version! Please read on if you enjoy “the story” behind the scenes.

Enjoy!

Myles

Brief History

While studying finance at the IU Kelley of School of Business, I met someone by the name of Kevin MacCauley. We went on to create the first ever collegiate-hosted half marathon in the country. We used the race as a fundraising vehicle for the largest cancer survivor scholarship in the country, which we created and had endowed at the IU Foundation. The first race drew in over 3K runners from all over the world and has given back hundreds of thousands of dollars to miscellaneous charities over the past 15 years.

Post-college, we both took corporate jobs in Chicago and began our careers. A new business endeavor took Kevin out to DC, while I remained in Chicago. A quintessential visionary, Kevin constantly had ideas that he was running by me. However, the pragmatist investor mindset in me shot most of them down. Eventually, we landed on a concept that we thought could change the landscape of youth sports, which was a marketplace to connect private sports coaches with parents & athletes: bookacoach.

In the summer of 2012, we both stepped away from our corporate jobs with zero capital raised and no technical background to begin building a technology business. Right at the corner of terrified and excited. Within a 6 month period, Kevin had lost his Dad and I had lost my best friend. However, we were still able to launch our MVP product in January of 2013. We were featured in Mashable, Techcrunch, USA Today and many other publications. We caught some initial early traction and grew the marketplace to a scale where I was able to get my hands on some data. What I found was that this was going to be a tough business, especially with some formidable competition in Boston: CoachUp (more on that later). However, there were a subset of customers that were using the application often and demonstrated strong KPIs. We conducted further customer discovery on this subset of customers and found that there was a bigger opportunity in producing software for sports facilities to better manage their operations. Upper Hand was born.

We pivoted the product and launched our sports facility management software MVP in late 2015. After running all facets of the business with Kevin in varying degrees, I ended up taking over the product team in 2018. It got me much closer to the engine of a SaaS business, which I loved. Leading the product team was the breeding ground for a key part of what would eventually become my investment process. Around the same time, the Techstars Sports Accelerator was announced to be launching in Indianapolis.

I immediately reached out to the one person that I knew that was involved, Scott Dorsey, to see how I could help. He quickly connected me with the MD of the program, Jordan Fliegel…the former CEO of CoachUp! Small world, and a key lesson on why you never burn bridges. Jordan has served as a key inspiration for me wanting to start a syndicate and fund.

I became involved as a mentor at first, and after becoming more involved, I was invited to join the team officially as an Entrepreneur in Residence. This was a pivotal moment. I took this opportunity to pull together a small group of friends that had either invested in Upper Hand previously, or that had shown interest in doing some venture investing, to form a closed syndicate. Below is a list of the original LPs:

Alex Cook: First 200 at ExactTarget and seasoned SaaS veteran.

Drew Swanson: Angel round investor at Upper Hand. Also Pre-IPO at Domo and Snowflake.

Marc Upchurch: Early Upper Hand investor & marketing guru.

Tyler Wilson: Angel investor & SVP industrial real estate broker.

When we were trying to figure out what to call our syndicate, the most popular name was “Hard Four LLC”, which was an extrapolation of Vegas experiences that we shared together. I continued to go down the path of what we all had in common and I landed on two things:

They all played a big part in my wedding, which was hosted at the Omni downtown Indy (Omni - Everything).

We all loved investing (Dollar - Money).

Everything money.

Enter…

The Omnidollar Secular Thesis

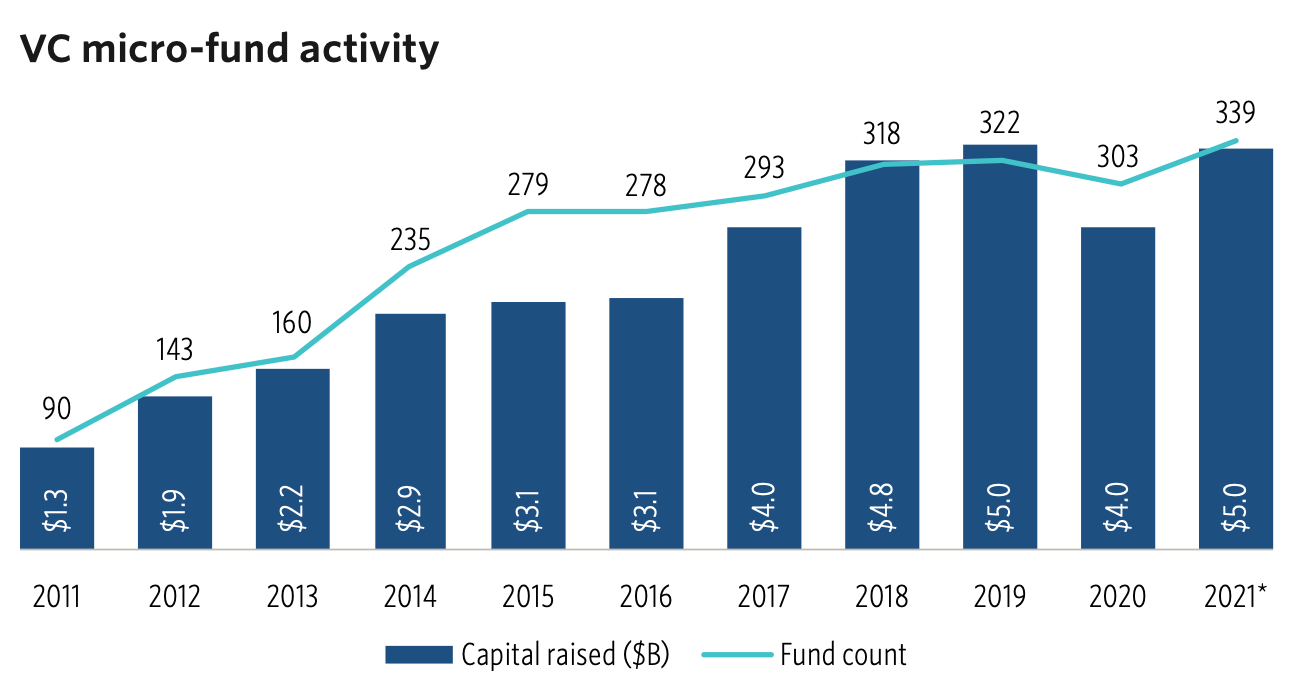

If you’ve read any of my pieces, you know that I am a thesis-driven investor. Put simply, I invest in and support innovative disruptors that are creating unstoppable secular shifts in consumer behavior. But this thesis-driven mentality goes well beyond my investments. Recognizing that time is our most finite asset on this Earth has led me to making time allocation decisions around this concept as well. As such, it’s probably no surprise that the Omnidollar Syndicate is rooted in a secular thesis that I see permanently changing the landscape of the Venture Capital ecosystem. A collision of new technologies born from Web 2.0 have broke down traditional barriers to entry for venture capital. This has led to an explosion of micro VC funds (fund sized <$50M):

Not only have there been an explosion of micro funds, but us “emerging fund managers” are found to be starting these funds 60% of the time (in some years 75%)! Last but not least, these funds are showing early signs of outperformance against our traditional counterparts:

Though returns data on micro-funds is thin, the sample data shows a strong return profile for micro-funds, which alone promotes confidence in their strategy. Coupled with the continued growth of these smaller vehicles and the growing proportion of micro-funds raised by established managers, micro-funds will likely perform well against benchmarks. (Source: Pitchbook)

The success of micro funds have now led to an explosion of Investment Syndicates. Traditionally, syndicates were run in the format of local angel networks or small hyperlocal, opaque investment groups. Now, with new burgeoning technologies such as AngelList, the traditional ways of raising capital through syndication have been disrupted. This disruption has created new opportunities for investors to gain access to early stage deals, but up until this point, most of the syndicates are being found in the coasts. I plan on changing that.

The Opportunity

From 2020-2021, we made 6 investments into companies produced from the Techstars Sports Accelerator program. While building this small portfolio, I started to realize that there was a lot more demand within my network to participate in deals like this, but they simply lacked two things:

Access to great deals

Someone they trusted to source & vet the deals

I made an assumption that this problem spanned beyond just my network. With new technology such as AngelList, I was able to solve both by opening up the Omnidollar syndicate to all credited investors that would like to participate.

Ultimately, I strive to solve three major problems with the Omnidollar Syndicate:

Deal Access: I’ve heard this time and time again: “I want to get exposure to venture capital, but I don’t know anything about early stage investing.” Or this… “I don’t want to write the check size for the venture capital funds.” I can solve that problem by leveraging my industry connections & experience to source high quality, early stage deals.

Founder Storytelling: As an entrepreneur, I know that telling your story can be extremely difficult. By combining great storytelling with the investments that I make, I can help founders tell their story in ways that they could not do on their own. This leads to wider product adoption and cheaper capital in the future.

VC Transparency: With inspiration from firms such as Ark Invest and

, my goal is to literally take the cap off of my brain and allow unprecedented access into how I make investment decisions. I want to continue to push the VC community to be more transparent with their investments. I believe that more decentralized decision making will ultimately rise the tide for all capitalists and entrepreneurs.

Anyone that wants to copy me, I hope that they do and I hope that they succeed. As new technologies continue to make it easier for entrepreneurs to create new concepts, we simply need more capital to invest in these brilliant entrepreneurs. Historically, this has been done by existing VC firms getting bigger or launching new funds. This leads to centralized decision making and many companies that should be funded, not getting funding. Furthermore, as capital continues to grow, we simply have more entrepreneurs being created from our economy. We need these founders to continue to create new businesses that improve our World, but we have an equal need for them to create their own funds. You can’t have the egg without the chicken.

Put simply, we need more emerging fund managers to continue to sustain the technological growth that our society needs in order to thrive. I think the best recipe for doing this is by spreading out access to amazing deals well beyond the limited number of individuals who typically have access to invest in venture capital funds.

The Elevator Pitch

Omnidollar is an early stage (pre-seed & seed), industry agnostic investment syndicate, with a primary focus in Sports, Fitness & Wellness Tech. I have a broad thesis that allows me to cast a net wide enough to ensure solid deal flow. However, I’m focused enough that it gives me a competitive advantage to capitalize on over a decade of industry experience. In addition to the deep domain knowledge within these industries, being a long-time founder & operator has enabled me to build tremendous networks in the venture & growth capital markets.

Multi-year/decade long secular shifts in consumer behavior ultimately drives my investment theses. This is the foundation of everything I do. Without this type of tailwind, I won’t step into an investment. Even though I am young by age, I have always, and will always continue to invest with an extremely long-term perspective. While I am not opposed to companies exiting early if the right opportunity presents itself, when I invest in a company, I expect significant tailwinds for a 5-20 year period.

Once I flag a secular shift that I feel has legs, I use deep domain knowledge of my focus verticals to triangulate the biggest opportunities within each thesis.

As an early pioneer in the sports & fitness tech space, I use nearly a decade of operating experience to vet deals, finding the strongest management teams that I feel are best poised to capitalize on the secular shifts. Within management, I look at a composition that has proven capabilities to develop unfair advantages and superior products. While this is difficult to gauge in the pre-seed stage, I have proven thus far that I am able to pick winners even when some management teams have little track records.

Due to the fact that I have nearly a decade head start on most investors in the Sports & Fitness Tech Space, I have developed & fortified strong relationships with some of the top investors & accelerator programs in the World. Mainly, with Indianapolis serving as home to the first ever Techstars Sports Accelerator program, I’ve been first in line to some of the best sports & fitness tech deals in the World.

Investment Approach

A common question that I have been asked as I’ve circulated Omnidollar amongst the investment community is, “What is your thesis?”. It’s another way of asking what’s your investment focus. The idea is that you look at the world in a very specific way to weed out noise (investment opportunities) at the top of your funnel so that you are able to efficiently focus on deals that only fit your thesis. You should save time and potentially select better investments, but the risk is that you pass on great deals that don’t fit your thesis. While I mechanically understand why investors approach investing this way, I don’t agree with it.

Ultimately, I’ve applied key learnings from the 6 investments that we made in our initial portfolio, my deep history of public investing, my decade-long run as a founder and all of the investment opportunities that I’ve passed on over the years to come up with the following approach. This was the first time that I put pen to paper on the approach and landed on the Omnidollar Investment Pyramid:

Secular Shift: It’s very difficult to find category creators that eventually become category definers. These are extremely rare opportunities that many times are riding the wave of a new technology that now enables them to change the way consumers operate in a specific function or vertical. These secular shifts create unstoppable tailwinds for businesses, making it much easier to scale, sometimes without even having product market fit.

Opportunity within Secular Shift: Once I have determined that there is either a secular shift already occurring, or I see one coming downfield, I isolate the biggest opportunities within the secular growth thesis.

Quality of Management Team & Product: Having operated in the past, I know firsthand that team is everything. Without a special team that complements each other well, there will never be an amazing product. However, in a hyper competitive environment, the most proficient product will always win. Even when there is little to no competition within a market, if I am picking the right secular growth theses to invest in, then the competition will come. It’s critical to me that the team & product are top notch as a result.

Unfair Advantage: Building a company from the ground up is incredibly difficult no matter what. However, the path is much easier when you have an unfair advantage. While it’s not critical out of the gates, I want to invest in companies that have a clear path to developing an unfair advantage.

Below are deeper dives on two of the layers of my approach that I have learned a great deal about during my previous investments and that have shown early signs of being critical to successful investments.

Unstoppable Secular Shifts

What makes my investment approach unique is that I reverse the traditional VC investor approach and will technically look at any business as a potential investment. Instead of looking at the deck or pitch and quickly batting it down due to it “not fitting my thesis”, I reverse engineer the opportunity to understand if they have the key foundation to making an investment:

Flagged Secular Shifts: Does the business fit an unstoppable secular shift in consumer behavior that I have already pinpointed? This is where I’ll spend most of my time actively sourcing deals.

New Secular Shifts: Does the entrepreneur have a strong likelihood of creating an unstoppable secular shift in consumer behavior? These are much more difficult to assess, but I also feel this is where most investors miss.

This is the foundational layer, and without an unstoppable secular shift being in place, or a high likelihood that the technology/founders are on their way to creating one, then we simply won’t invest. Over the years, one of my key observations is that these secular tailwinds can take time and require patience. I’ve also learned that as market dynamics change, my secular theses can change as well. Patience is important, but equally important is admitting when I am wrong, as this eliminates doubling down on mistakes.

Unfair Advantages

Having an unfair advantage is many times what sets aside the good from the great. As I constantly assess Omnidollar’s current investment portfolio as well as companies that I passed on, these unfair advantages continue to play big roles in the early success/failure of a company. Here are a few key learnings that I am using to assess deals now, that I didn’t know when I first began investing in early stage companies:

Founders Role & Time Decay: As my time invested in theses companies continues to lengthen, I am learning that the quality of the founding team is critical in ensuring that new unfair advantages are created. If a founder sleeps on an unfair advantage and lets their guard down, this opens the door for competition to creep in and tilt the table. Put simply, there is a time decay on these unfair advantages, and I am seeing that the great management teams are able to better lengthen, or create new, unfair advantages.

Accelerators & Venture Studio Companies: Ironically, a big part of what I have considered an unfair advantage for Omnidollar (plugged in to accelerators such as Techstars) is equally, if not more, advantageous for the companies coming out of these programs. Not only are key learnings accelerated at a critical inception stage, the vertically-centric programs are getting really, really good at adding value through key resources & relationships. Companies coming out of these programs have significant unfair advantages relative to their competition.

Defensibility: This, like many aspects of investing at pre-seed stage, tends to be very subjective analysis. However, sometimes the defensibility of an unfair advantage can be pretty clear, cut and dry. For example, if a company has a key patent issued that blocks out competition for a set period of time, this is clearly defensible. On the contrary, the unfair advantage of coming out of a top tier accelerator or venture studio will weaken at a certain point.

In summary, the best companies that I have invested in/passed on share the same characteristics. The top early stage companies are powered by strong, product-centric management teams, with unstoppable secular shifts and unfair advantages.

Investment Portfolio

In developing the initial investment portfolio, the key learnings have been rich. When I first started making early stage investments, I had no specific approach to making investment decisions. The successes and failures of the initial portfolio have helped me to craft and fine tune my investment approach. They’ve also helped me realize how I can differentiate Omnidollar in what is still a very competitive capital market. In traditional venture capital fashion, our portfolio has ranged from a 13x return to one of our companies shutting their doors. However, the overall portfolio remains very strong with solid mark-ups and tremendous long term opportunity. Below are some highlights:

Ergatta: Raised $30M at a $200M post-money valuation. Omnidollar participated in the Seed and Series A rounds.

Project Admission: Anthemis led their Seed Round of $5.5M at an undisclosed valuation. This resulted in a generous mark-up for Omnidollar

Tennibot: Raised their Seed round led by Benson Capital Partners. Omnidollar participated in the Pre-seed round.

While Beastcoast and Locker have yet to hit any key fundraising milestones since we invested, they continue to demonstrate great progress in building their businesses.

Moving forward, I plan on doing deep dive public investment memos on all of my syndicate investments, but I’ve done two which can be seen here:

Deal Flow

As I’ve gained more and more experience doing VC investing, I’ve been able to distill the industry into what I call “The 3 Ds”:

Dollars: How are you going to fund companies? Are you going to raise a fund, syndicate deals, do angel checks, etc?

Differentiation: How are you going to differentiate your fund both from a fundraising perspective, and from attracting top companies from other more established funds?

Deal Flow: How are you going to fill the top of your funnel with incredible deals to choose from?

They are all very difficult and complicated prongs, but the last one has been incredibly challenging the past few years as capital markets have been extremely competitive. However, I see the last two as being very closely tied. Here’s how I am leveraging differentiation to increase deal flow:

Previous Founder: The fact that I am a previous founder and am not sitting on 10 boards/inundated with running a $50M fund, I am able to add tremendous value to founders, especially in a key area (product). Being a previous founder allows me to see eye to eye with burgeoning entrepreneurs and display an incredible amount of empathy toward them. When I tell a founder that I want to partner with them, it’s not just a transaction to me and they know it, because it’s the truth.

Techstars: I am leveraging my existing network within Techstars to get my eyes on companies that already have an established unfair advantage. Given that there are 3 sports accelerators (2 in the Midwest) produced by Techstars, there’s ample strategic deal flow throughout the year from these programs alone, but I plan to continue to expand my network to the other more successful programs.

Strategic Contacts: I have begun building my strategic deal flow network throughout the globe. I am generally looking for someone that I know or a warm referral that has an intricate sense of the start-up ecosystem in cities that I have flagged as strategic ecosystems. I have partner documents drafted with them to do a carried interest share to encourage them to source the best deals for me.

As I continue to source great deals and provide uncanny support to the founders that I back, deal flow has already began to increase. This is without a doubt, a very key function moving forward as I continue to make Omnidollar a premier location to obtain growth capital for extraordinary entrepreneurs.

Investor Details

If you’re interested in investing, below are some key details:

Risks: You should not invest anything that you aren’t willing to lose. Early stage investing is incredibly risky. Please consult your financial advisor as I am not a registered investment agent.

Legalities: Technically, you should be an accredited investor in order to participate in these deals. Consult your legal counsel to understand if you’re accredited.

Fees: There will be no management fee on the syndicate deals, but there is a 20% carried interest on all deals. This fee is standard in VC investing and is essentially to align incentives for GPs with LPs. AngelList also charges $8K per deal for technology fees and the formation of the legal entity used to invest. This fee is split proportionally based on your investment percentage.

Platform: I am using AngelList as the main platform to introduce deals to my LPs. If you’re not signed up on AngelList through this link, you won’t see the opportunities to invest. Please share this with anyone in your network.

Typical Minimums: Generally, the minimum investment amounts will be $5K, but this may change depending on the deal.

Deal Stage: I generally invest in pre-seed and seed rounds, but if great deals are introduced at a later stage, I may bring those opportunities to the syndicate as well.

Investment Life: Because I invest early, these are long-term, illiquid investments. Plan on your capital being illiquid for 5-10 years. Until there is some sort of exit event such as the company being purchased or going public, it’s impossible to get your capital out.

Deal Leads: When possible, I want to source deals that have a VC lead. However, in the pre-seed stage, this can be difficult to find. In the event that there is no VC lead, I will look for participation from an accredited accelerator or VC firm. Otherwise, I likely will not bring the investment to the syndicate network.

The Future

There are a handful of interesting concepts that I am very bullish on as it relates to investing (studio models, implications of DAOs, etc.), but I am most bullish on the secular rise of emerging fund managers. There’s a strong need for them in the entrepreneurial & VC ecosystem. Combining founder-inspired content, syndication and a micro fund into one flywheel is my ultimate vision for Omnidollar. My intention is to back incredible founders with expertise, inspiration and capital as they go on to break down historical barriers, whatever they may be. By opening up the Omnidollar syndicate, my hope is to allow you to have a seat on the incredible journeys that these entrepreneurs create. As my journey as an investor continues to unfold, I look forward to producing access to great deals and educational & inspiring content around these founders & their businesses. I’m beyond excited to open a new, fresh door to the VC & entrepreneurial community. Welcome to Omnidollar.

If you have any questions, please feel free to email me at myles@omnidollar.io to discuss more.